")

Wealth without budgeting or sacrifice

In Part 2 we looked at some steps to build wealth and to stop worrying about money. We talked about tracking our wealth as a key step and got our head around the power of compounding. Specifically, how to get it working for us rather than against us. Then we considered how to convert our joy of shopping to a joy of wealth building. We saw the power of a reduction in a recurring expense and the wealth that can build over time.

In this section, let’s look more at some examples of spending changes and some other easy tweaks and the effect they can have on reducing our money worries.

Mindful spending on discretionary things

I was watching Marie Kondo on Netflix a few nights back (don’t ask) and she was busy “tidying up” someones house. To the uninitiated that means examining each item in one’s home, in a special order, and discarding that which “doesn’t bring joy”. In a typical episode, she banishes dozens of garbage bags of joyless matter to reduce clutter and improve the positive juju in the home. While the houses look much better after she completes her craft, it does beg the question…What if people never bought all of that stuff in the first place?

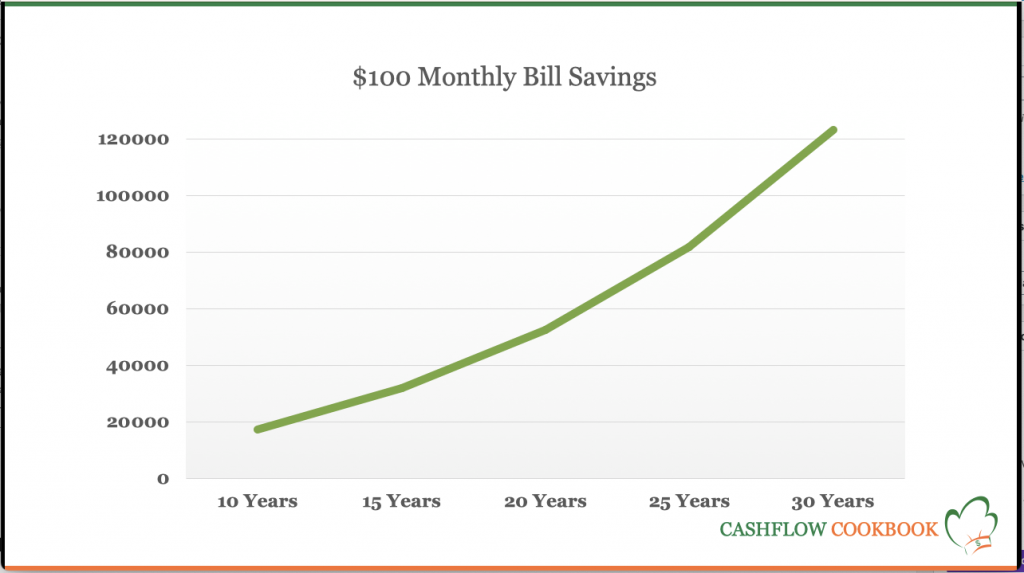

Clothing is a popular item since people typically only ever wear about 25% of the clothing they buy. The rest hangs out (literally) in the closet for a few years, then makes a trek to a yard sale or a thrift shop. Is that a big deal? In a typical Tidying Up episode, about a dozen garbage bags of clothing are removed. Let’s say there are 20 items per garbage bag and lets say each item cost $50. So about $1,000 per bag, or $12,000 in total. Say each haul accumulates every 5 years which means that we are wasting about $2,400 a year or $200 a month. What happens if we invest that at 7% over, say 30 years?

Looks like it adds another $250,000 of wealth. In part 2, we saved $100 a month by renegotiating one of our regular bills and that added close to $125,000 of wealth over the same period. So with a couple of easy tweaks, we added $375,000 of wealth over a 30 year period. So we have have nearly doubled the retirement wealth of the average North American with a couple of changes. In other words, we have started building wealth without budgeting or sacrifice.

But I want to get rich now!

This begs the question, “What if I don’t want to wait 30 years to become rich?”. There are a few answers to that:

- If you start working at 23, 30 years later, you are only 53 and statistically, you still have about 35 years of life ahead. Better to enjoy those years with the extra $375,000 than without it. You will particularly think that way when you reach that age.

- We are just getting started with a couple of ideas. What if you could find $800 a month of savings that you invested? That would add another $1 million to your stash.

- What you do with the incremental wealth is up to you. Pay down debt faster, increase your investments, donate it to a school in Kenya, or retire early and launch your singing career. The point is that these changes give you options and freedoms.

- Maybe the most interesting point is that you didn’t have to work harder to gather this $375,000 and you didn’t have to give anything up. You spent an hour on the phone with a service provider and whittled down a bill, and you got a little more mindful on your clothing shopping. Actually buying things you needed rather than buying something, returning home and seeing 4 of them hiding in the back of your closet.

- Notice too that we built all this wealth without budgeting or sacrifice. And no spousal arguing. So far.

Small income boosts make a big difference

Let’s say you have a household income of $100,000. Here in Ohio, that brings in about $6,000 a month. If you were able to save $1,000 a month that would be 12% of your gross. Let’s assume that the rest of your bills consume the other $5,000. (You can grind those down easily with some of the ideas here.)

If you could earn an extra $12,000 a year after tax, that would double your savings rate from 12% to 24%. Over a 40 year career, investing that extra $1,000 per month would add an extra $2.6 million to your wealth. Or let you retire a lot sooner with a lesser amount. Where does the extra income come from? Applying work raises to savings vs increased consumption, a rental property, a moderately successful blog or any of hundreds of other ways of extra earning. Do a bit of Googling on that.

Note that the original $1,000 of monthly savings could also grow to $2.6 million over 40 years for a total of $5.2 million at retirement. And nothing to say that there may not be another $1,000 a month that could be saved and invested from within the original income. And all this works if you are making $200,000 or $50,000, just scale the numbers to suit.

Improving your investment returns

Through all of this, we have used 7% returns in doing the math. I am often asked why I use 7% when bank savings accounts offer next to nothing in returns. The answer is that you need to have investment returns well beyond those offered in bank savings accounts to build any kind of wealth. With no real investment returns, inflation will gobble up the value of your savings. The average return on the US stock market over the last several decades is about 8%, so 7% is not unreasonable. In an earlier blog post, I offered some ideas on how to exceed that by partially investing in a basket of stocks that are aligned with current trends. All of the stocks that I mentioned in that blog have continued to soar. But aside from stock selection, there are plenty of low risk ways to improve your returns including:

- Not getting in and out of the market based on news headlines. Time in the market beats timing the market. invest for the long haul.

- Not acting on hot tips from Uber drivers, Reddit forums or dentists.

- Being sure to diversify your holdings by industry, geography and investment type.

- Tracking your investment returns each year and knowing whether you are beating the market indices of each asset class.

- Keeping your investment costs low, and especially avoiding the issue of high investment fees and returns that lag the market.

- Aligning your investment mix with your life age and stage, your risk tolerance and your

So how much of a difference does the return percentage make? As we looked at earlier, at 7% a monthly investment of $1,000 over 40 years will build to $2.6 million. Increasing the return to 8% yields a nest egg of nearly $3.5 million. Wow.

Summary

- Look for ways to reduce recurring expenses.

- Shop more mindfully and sidestep buying things you would never use.

- Look for ways to increase income.

- Apply the freed up funds from 1, 2, and 3 to debt pay down or incremental investment.

- Understand your investment returns and avoid the usual pitfalls that lower returns.

Part 4 looks at a whole other gearshift to build wealth. It’s one I didn’t really understand until later in life.

What have you done to build wealth more quickly? Let me know in the commentsWealth without budgeting or sacrifice.

Photo credit Mohamed Nohassi at Unsplash

")

")