Looking for a way to reduce loan interest?

In a perfect world, we would just pay cash for everything. But sometimes you just need a loan. Maybe you need cash for your business, or Elon wants you to invest on the ground floor of his new company. Perhaps you just need funds for a car or other asset. The compounding effect of borrowed loot is nasty, so it makes sense to look for a way to reduce loan interest.

One obvious approach is to do a bit of haggling. On a mortgage or a car loan you might be able to shave off a quarter or a half a percent of interest. Worth a try. Or you could try shopping the loan between some different lenders, banks or credit unions. For mortgages, working with a licensed mortgage broker can get you a better deal than your own shopping. Sometimes attractive financing can be had from the people trying to sell you the asset – like the Ford dealer at month end, in a blizzard, in January, during a recession. All of these are worthwhile, but for the really big savings, you’ll want to dig into another approach. And it’s one that I didn’t really understand until just recently, even after buying 9 houses and about a dozen cars over the last 40 years or so. How much did I overpay on those loans and mortgages? Ugh.

The power of your credit rating

Sure, we’ve all heard of credit ratings – those numbers that tell lenders how likely we aren’t to pay things back. They run on a scale from 500 to 850. But how much do you really know about them? I don’t think I ever knew my number or what it meant until my recent move to the USA. Back in the old country, I had lots of credit cards and an awesome limit. In other words, a great opportunity to collect points for fabulous cash and prizes. But when I tried to open a Best Buy credit card here in Ohio, my application was rejected. Whoa! What! Bit of a blow to the ego. Turns out credit records don’t cross borders. I was starting from scratch like a new graduate, but with grey locks, wrinkles and a middle aged body. The worst of both worlds. So I was forced to begin with a bank credit card of $300. Wait for it…secured by $300 that I had to keep on deposit! And those cards don’t earn points. Humbling!

After a few months of carefully paying off my junior card, my credit rating went from 520 to 750. Not bad. Soon I will be able to remove my card training wheels and liberate my $300. Now, new credit card offerings arrive almost daily. And now some of them have points. I’m back!

Good to have credit cards with normal limits, but I got curious and started to learn more about credit ratings.

Credit ratings to the rescue to reduce loan interest

Turns out that your credit rating makes a difference on your loan interest rate. Like a very large and massive difference. Over at myFICO they have a nifty calculator to show just how big a difference your credit score makes on your loan interest.

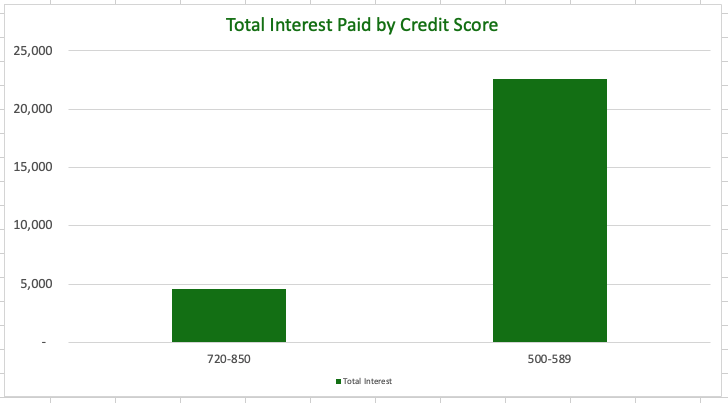

As an example, considering someone buying a new F150 pickup truck for $50,000 on a 60 month loan. How much would the payments be? It depends. Looking at the myFICO calculator, they could be as high as $1,209 a month or as low as $909 a month. The total interest cost over the 60 months could be $22,552. Or as little as $4,567. Hard to believe. But true! It all depends on your credit score. Turns out having a great credit score is a key way to reduce loan interest.

The high payment and interest figures are for a borrower with a credit score of 500-589. Could be someone new to the country (been there), or someone who missed some payments or is carrying a lot of debt. The low payment and interest numbers would be experienced by someone with a strong credit score of 720-850.

Sounds like it is worthwhile to learn about credit scores.

Credit scores are set by the 3 major reporting agencies: TransUnion, Experian and Equifax. Each of them receive information from lenders about your payment history and credit limits as well as public information about you, such as bankruptcies. They then score your file and make that information available to other lenders and/or sell it to companies who want to present you with things you don’t need (like all of those pre-approved credit card offers that line your iguana’s cage.)

You can get your credit score for free at annual credit report or sometimes from the credit companies themselves. Experian, as an example provides your score if you set up an account with them. Each of them offers more advanced services which they enthusiastically sell you at every chance they get. Your bank may also be willing to provide your score as well. To reduce loan interest you’ll want to find ways to improve your credit score.

My credit score isn’t great. How do I improve it?

There are several factors that the credit companies use to evaluate your score including:

- Your payment history

- Credit use

- How long you’ve had your credit

- Credit mix (do you have different kinds of credit such as credit cards, mortgage and car loans)

- Application for new credit (new cards, mortgages, car loans etc)

To improve your credit rating, you need to improve some or all of these factors. Pay the balances in full when they are due, stay under 30% of your total credit limit, cancel cards that you aren’t using, and don’t apply for new credit unless you actually need to. Also check your credit report for errors and get them fixed. Sometimes they will show you as having cards that are long gone, as an example.

Summary

Credit scores are easy to ignore. According to a recent GoBankingRates survey, about 40% of Americans don’t know their credit score. It follows that many people don’t realize the effect that it can have on an opportunity to reduce loan interest. Take the time to learn your score and improve it. This is important if you are thinking about a loan, but even important when you aren’t. Good to be ready should you need access to some extra cash for an emergency or a worthy cause.

I should also mention that rushing out to buy a brand new truck with a loan isn’t likely to be the best financial decision. Especially if you’ll only be using it to carry your lunch and not heavy gear like the dudes in the picture. Buy the vehicle that you need for 90% of your driving. Rent something else for the rest. And a 2 year old used vehicle can represent great value. Learn more about how to buy the perfect car.

And of course, the $17,985 in reduced interest could be put to very good use. Over 40 years, invested at 7% it could grow to a tidy $287,760. Not a bad addition to your retirement account. For $13,000 of monthly savings ideas, check out the book.

What tricks do you have to reduce loan costs? Let me know in the comments.

Photo credit Said Al-Olayan