How to control your spending?

It was shaping up to be a financially prudent month. Until you checked the bank statements. A few “dangs”. A handful of “ugh, forgot about that ones”. And some “what was I thinkings?”. Oh, and that was before viewing those 2 other credit card statements. Sadly they all added up to make your month fiscally regrettable. Wouldn’t it be handy to have a list of spending considerations to apply before giving your credit cards a workout? A pre-spending checklist. A kind of monetary mom to control your spending.

In fact, there is! Here are some ideas to control your spending with minimal effort or sacrifice:

Shop mindfully – lead us not into temptation

The science of shopping has developed immensely. Every aspect of retail is fine-tuned to make you spend. The lights, colors, music, product placement and last-chance urgency are all there to fill your cart. Store sensors are monitoring where you move, what you buy and where your eyes look. MRI testing reveals what merchandising and messaging lights up our internal “buy buttons”. Heading to the mall with no real needs is like swimming with the sharks. While wearing a meat swimsuit.

Instead, shop mindfully. Shop when you actually need something. Bring a list to the mall or to your laptop of exactly what you are looking for. Double-check that you don’t already have the thing at home – hidden under the couch, in the attic or in your closet.

Set a cooling off period – desperate needs become vague wants

Marketers do everything possible to create passion for their products and drive urgency into your buying process. If the item isn’t an urgent necessity, give yourself a little cooling off period to regroup. Consult with some friends to get their thoughts. See if your Dad thinks it’s a good idea. Set a calendar reminder to see how important the item still is in a couple of weeks. This is often referred to as “the thirty day rule”. In Quora, someone asked me if there is a shorter version of the 30 day rule. Weird question. I suggested the 15 day rule. While you are waiting the 30 or 15 days, spend some time glancing through your credit card bills and account balances to temper your spending desires.

Can you share or borrow one to control your spending?

If the thing you need is large, heavy, expensive or will be rarely used, think about buying it with a neighbor and sharing the cost, maintenance and maybe even the storage. I did this for years with a snowblower. My next door neighbor, Peter and I split the cost, shared the maintenance and took turns plowing each other’s driveway. Way better than us each buying a machine and plowing solo. This idea works well for power washers, table saws, Spiderman costumes, chainsaws, prom dresses and dinosaur cake molds. Less effective for linens, stuffed toys, floss or pajamas.

Can you rent one?

Hello gas powered post hole diggers, drywall hoists and wedding dresses. And believe it or not, even caskets, camping gear, goats and luggage. The cost savings can be considerable – e.g. caskets rent for about $750 vs $5,000 to $20,000 to buy. Renting seldom used items can also free up a lot of storage space. How often do you use all of the gear that lines your garage? Renting things you might have bought can be a good way to control your spending.

Can you get a used one?

If you kind of need the item around all the time (like kids, dishes or pets) borrowing or renting likely won’t do. You may need your very own. There are tons of marketplaces to do that. Reverb for musical instruments, Poshmark and Tradesy for used fashions and Craigslist, eBay, Offerup, Facebook Marketplace and Letgo for everything else. Most of my guitars I bought used, typically in mint condition and saving more than half. Or allowing twice as many guitars.

Get the best product

For products, Amazon reviews are great even if you don’t buy from Amazon. Their process limits the reviews to actual purchasers and the large numbers help with accuracy. One of the all-time research bargains is ConsumerReports.org. Sign up for an online membership for $30/year. Completely unbiased reviews of everything from snow tires to sun screen, tractors and strollers. Makes sure you have a product you enjoy, saves on repair costs and the hassle of replacing it before its time.

Make sure you aren’t overpaying

Once you figure out that you really want, but also need, a thing, do your research. On home renovations, there are lots of ways to save. Shopping around is a powerful use of your time. It works on just about everything. A couple of weeks back, I realized that CashflowCookbook.com was running too slow. A local company offered to speed it up for $3,000. A quick online post introduced me to a highly-rated Australian company whose specialty is speeding up WordPress websites. Boom! Their premium offering is all of $495. They did a stellar job and left me with an extra $2,500 in the bank. On the consumer side, there are dozens of sites that focus on comparison shopping on your behalf. Here is the amazing results of my car insurance shopping project. Lots of comparison sites for anything else you need to buy. Check out Google shopping, PriceGrabber and shopping.com.

How do you control your spending? Share your tips in the comments below.

Photo credit Ellie Burgin on Pexels

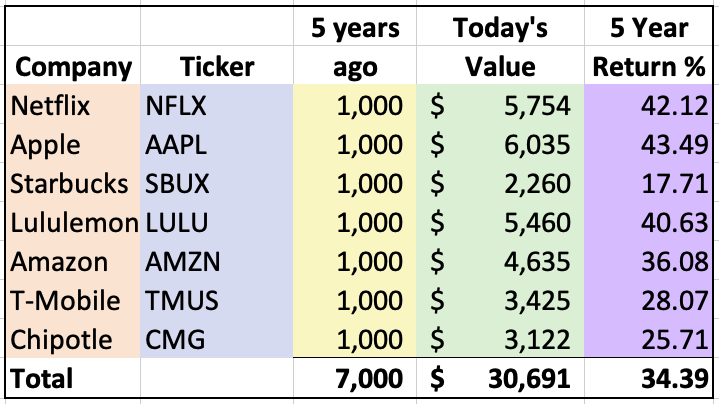

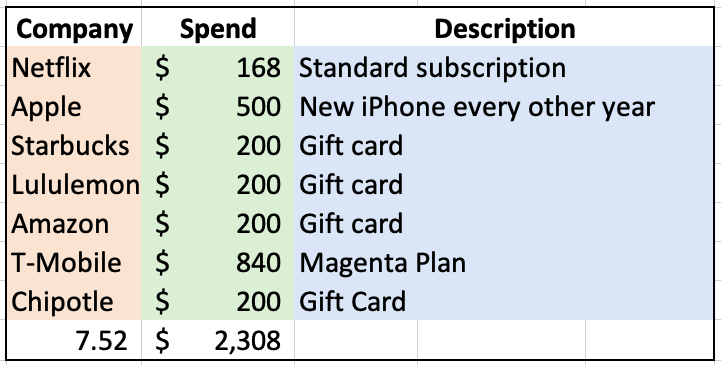

So we will start with a new iPhone every other year for $1,000, or about $500 per year. Let’s add a cell plan and let it gorge on unlimited 5G data. Tasty. Tuck in a standard Netflix subscription. That adds up to $1,508. Then let’s spend $200 on gift cards from each of Starbucks, Lululemon, Amazon and Chipotle. That all ads up to $2,308 of fun stuff every year. Some nice lifestyle additions. Why those numbers?

So we will start with a new iPhone every other year for $1,000, or about $500 per year. Let’s add a cell plan and let it gorge on unlimited 5G data. Tasty. Tuck in a standard Netflix subscription. That adds up to $1,508. Then let’s spend $200 on gift cards from each of Starbucks, Lululemon, Amazon and Chipotle. That all ads up to $2,308 of fun stuff every year. Some nice lifestyle additions. Why those numbers?